Hoxton Whitepaper: Europe’s “Sputnik Moment” in AI – And Why It’s Still Crucial to Win the U.S. Market

Five factors to grow 25x bigger by succeeding in the U.S.

Executive Summary

Europe has the opportunity to generate a “Sputnik moment” with artificial intelligence, recalling that pivotal moment from 1957 when the Soviet Union shocked the U.S. The continent boasts top academic institutions, globally recognized AI talent, and a growing cohort of high-value start-ups.

Historically, despite the intellectual capital and technological promise, Europe has lagged the U.S. in commercial outcomes. However, this is changing. Europe represented less than 5% of all unicorns created globally in 2017 and today represents 20% in 2025 YTD. That said, the largest multi-billion dollar venture scale outcomes are still dependent on winning in the U.S.

Of course, every company has unique circumstances to consider and European founders in particular must think about the following strategies on a case-by-case basis to increase their chances of delivering a venture scale outcome:

-

- Moving to the U.S. as early as possible, once financially and personally feasible

- Tailoring product for the market

- Building early commercial traction with local reference customers

- Raising money from U.S. venture firms

- Listing in the U.S. and building relationships with prospective U.S. based acquirers

Europe has the research pedigree and talent to lead the next wave of AI innovation. Winning the U.S. market doesn’t make you less European – it increases the likelihood of building a global category leader.

Europe’s “Sputnik Moment” in AI

Europe has emerged as a foundational hub for artificial intelligence research and innovation. Europe is home to some of the world’s top AI institutions – University of Cambridge, University of Oxford, ETH Zurich, Technical University of Munich, Imperial College London, and University of Edinburgh, among others.

Why the U.S. Remains Central to Commercialization

With $18.8T in household final consumption expenditure (HFCE) in 2023, the U.S. is nearly double that of the EU and almost triple the size of China. For technology companies building global platforms, product-led growth or enterprise sales channels, the U.S. remains the single most important battleground.

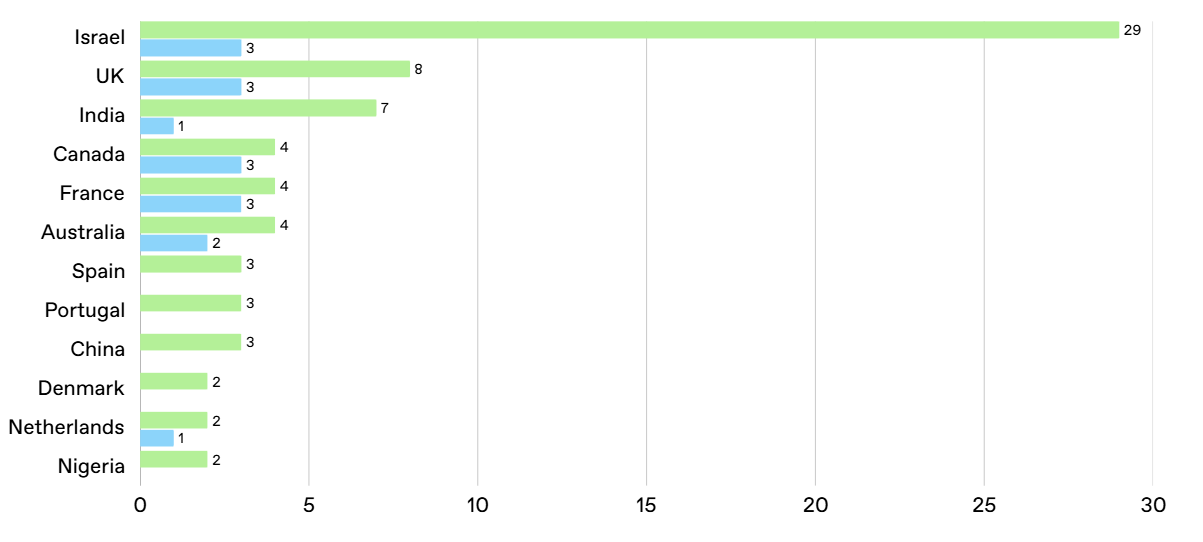

Relocating to the U.S. has historically boosted the chances of a startup achieving unicorn status. Based on Prof. Ilya Strebulaev’s research, startups relocating to the U.S. from Israel were 9x more likely to become unicorns (1997–2021), India 6.5x more likely, UK 2.5x, Netherlands 2x and France 1.3x3.

Internationally founded U.S. unicorns

Why the U.S. Matters When Raising Capital

Simply said, there is more capital available in the U.S. The U.S. attracts 6x more VC funding than the next-largest market (China) and based on Sifted’s latest Transatlantic Founder Survey, European founders find it almost twice as challenging as their U.S. counterparts to raise – 53% vs 30%, respectively.4

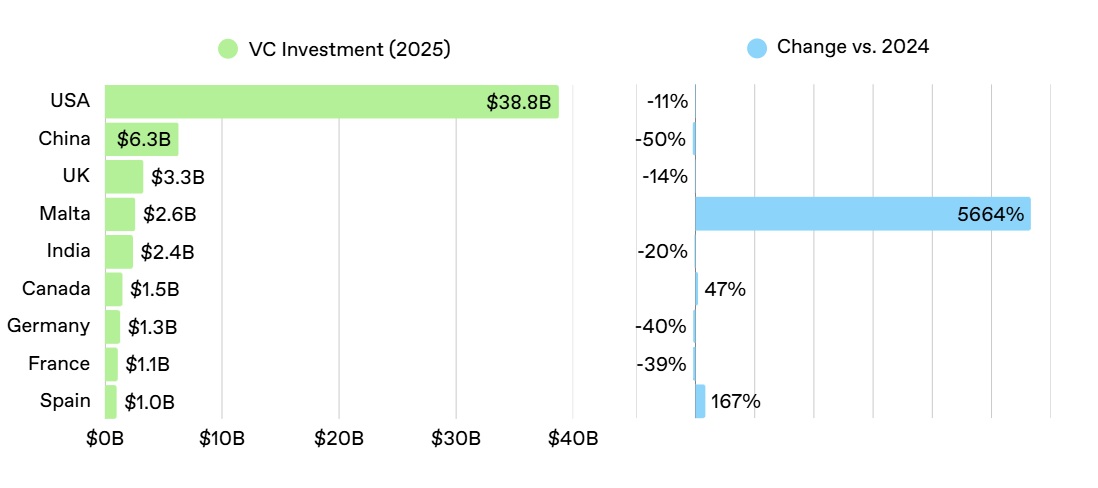

In 2025 thus far, VC funding in the U.S. is $38.7B while China follows with $6.5B and the UK $3.88. Altogether, Europe totals more than $9.OB, elaborating the importance of aggregating resources.5

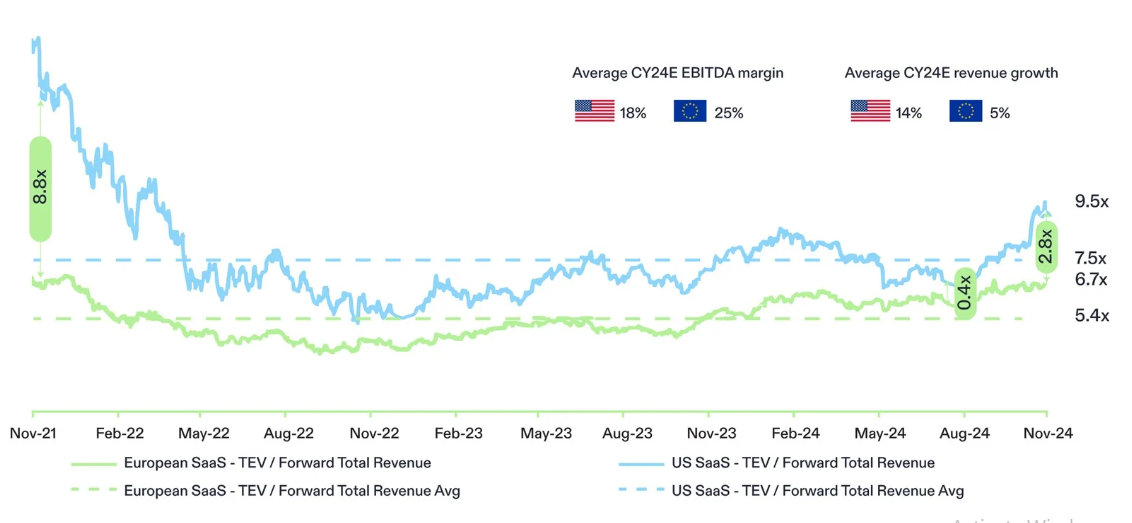

Further, companies in the U.S. attain higher valuations at larger round sizes. U.S. SaaS companies command 20%-40% valuation premiums over their European peers (9.5x vs 6.7x EV/Revenue multiples).6 The gap has widened post-2023.

For founders, this translates into larger rounds, higher valuations, and better terms in the U.S.. And larger rounds correlate to higher probability of building a unicorn – “at seed stage, future unicorns raise on average $9M vs just $2M for average startups. By Series C, unicorns secure on average $105M compared to $27M. The gap widens in later stages, with unicorns raising on average $304M at Series G versus $66M for others. And in the U.S., startup valuations and round sizes remain significantly higher – roughly 40-100% above their European counterparts at the same stage.”

For founders, this translates into larger rounds, higher valuations, and better terms in the U.S.. And larger rounds correlate to higher probability of building a unicorn – “at seed stage, future unicorns raise on average $9M vs just $2M for average startups. By Series C, unicorns secure on average $105M compared to $27M. The gap widens in later stages, with unicorns raising on average $304M at Series G versus $66M for others. And in the U.S., startup valuations and round sizes remain significantly higher – roughly 40-100% above their European counterparts at the same stage.”

Why the U.S. Leads in Exit Opportunities

Looking at M&A activity, in 2024 the U.S. value of dealmaking was $1.24T while Europe totaled $5248, up 25% from 2023, but still dwarfed by U.S. 9activity. The U.S. leads in both volume and value of strategic acquisitions, especially by Big Tech. European founders under-index their U.S. counterparts almost 2:1 when considering future acquisition or IPO plans and can benefit from being more proactive thinking ahead here.10

The U.S. has public market advantages as well. Looking at valuation premiums, U.S. companies consistently trade at -40% higher multiples than European peers (S&P 500 vs. STOXX 600).11

The U.S. has deeper capital markets with the largest base of institutional and retail investors. IPOs raise more capital, attract more liquidity, and enable easier follow-ons in the U.S. Global visibility is higher with U.S.-listed companies receiving more analyst coverage, institutional research, and international media attention – resulting in better price discovery and investor engagement.Companies are increasingly opting to delist from European exchanges to list in the U.S., capitalizing on valuation arbitrage and better investor access.12

The U.S. has deeper capital markets with the largest base of institutional and retail investors. IPOs raise more capital, attract more liquidity, and enable easier follow-ons in the U.S. Global visibility is higher with U.S.-listed companies receiving more analyst coverage, institutional research, and international media attention – resulting in better price discovery and investor engagement.Companies are increasingly opting to delist from European exchanges to list in the U.S., capitalizing on valuation arbitrage and better investor access.12

The Power Law of U.S. Outcomes

A recent DST Global study of companies with $5B+ valuations from 2012–2024 showed 116 companies reached this lofty threshold with 14, or just 12%, headquartered in Europe.9 European cities with multiple $5B+ outcomes were London (Wise, N26, Revolut, Monzo, Checkout.com), Munich (Celonis, Personio, Helsing) and Paris (Doctolib, Mirakl).

Looking at trillion-dollar technology companies, TSMC of Taiwan is the only one outside the U.S. to reach this status, generating 70% of their net income from North America.14

Outlier success – the cornerstone of venture returns – is disproportionately American. Founders with big ambitions must set their eyes on the U.S..

Case Studies from the Hoxton Ventures Portfolio

By design, Hoxton identifies and backs companies with the assumption they will go global when ready to scale. Headquartered in the UK, Hoxton invested in Darktrace in early 2015 before they expanded operations into the U.S. and began securing customers in 2016. In 2023, 35% of Darktrace’s revenue came from the U.S. – more than all Europe combined (26%). The U.S. is a critical revenue driver, even without relocation.